Digital Assets Service Providers: A new era for capital markets

Bryan, Garnier & Co technology equity research team is pleased to release the white paper Digital Assets Service Providers: A new era for capital markets which takes a deep dive in the EUR29bn market opportunity harboured in digital assets and tokenisation.

Our latest white paper reviews the market opportunities in the digitalassets services sector, as well as technological disruptions and challenges for the industry. Read this report to learn about the key technological and competitive trends that will shape the digital asset services market, and understand why we consider that technology providers could emerge as the major beneficiaries.

Request the report

Please complete the form below to receive the report.

KOL call: Idefirix for Kidney Transplantation

bethsabee gresse

Our guest

Autolus

BioNTech

Cellectis

Evotec

Galapagos

Date: Nov 22th from 2:00pm CET

Join our chat with a European KOL to learn more about the use, adoption, and potential of Idefirix as a desensitization agent in patients undergoing kidney transplantation.

Kidney transplantation is not an option for candidates with high concentrations of donor specific IgG antibodies (DSA). Their only shot at a transplant may be to eliminate DSAs via desensitization. Imlifidase trials showed that, for the first time, a desensitization agent led to rapid and complete antibody depletion, regardless of their initial strength or number. Imlifidase has been approved in Europe (Idefirix).

Idefirix provides a dramatic improvement to desensitization, should ultimately become a mainstay in high-sensitized transplantation, and will not be easily replaced.

Bryan, Garnier & Co Expands Software and Fintech Investment Banking team with new Managing Director Jean-Malo Dupart

Jean-Malo Dupart

Investment Banking

PARIS – 6th October 2022:

Bryan, Garnier & Co, the leading investment bank for European healthcare and technology-related companies, has announced that Jean-Malo Dupart has joined the firm as a Managing Director. Based in Paris, Jean-Malo joins Bryan Garnier’s software investment banking team where he will play a key role in continuing the bank’s leadership in the sector, particularly within fintech.

Jean-Malo has deep financial services experience, having worked at large institutions in both New York and in Paris across capital markets, structured credit and lending. He joins from Société Générale where he was part of the Corporate Development and Strategy team. At Société Générale, Jean-Malo spearheaded the bank’s M&A transactions and strategic investments in startups and fintech companies. Jean-Malo has completed numerous cross-border deals and projects across the fintech sector including within payments, digital lending, banking-as-a-service, crypto and digital assets, insurtech and e-banking.

Thibaut De Smedt and Stanislas de Gmeline, Partners within Bryan Garnier’s software team said: “We are delighted to welcome Jean-Malo to Bryan Garnier. He brings with him a wealth of experience, technical expertise in a variety of fintech segments and an extensive network of investors across key technology growth markets in Europe that will ensure our clients continue to benefit from sector-specific advice and flawless deal execution. His addition to the team will support our strategic ambitions and ensure we continue to build on our strong track record in software and fintech.”

Jean-Malo Dupart said: “Having been a client and a partner of Bryan Garnier in the past, I have always been impressed by the firm’s highly committed team, brilliant execution capabilities and relentless focus on understanding and supporting their clients to achieve their strategic objectives. With an excellent reputation in the technology market, a successful track record of supporting growth companies and their shareholders at all stages of their development and a global network of investors, the firm is well positioned to expand its presence in the fastest growing segments of the fintech industry in Europe and I look forward to playing a key role in the Firm’s continued growth in this sector.”

Bryan Garnier has advised on a number of fintech deals to date, including a private placement in Qred, Sweden’s fastest growing fintech company by Nordic Capital in September 2021 and a €25m investment in digital banking company Skaleet by US private equity firm Long Arc in December 2020. Bryan Garnier also advised Société Générale on its acquisition of French neo-bank Shine in June 2020, leading software investor Hg on its investment in smartTrade in February 2020 and Groupe Crédit Agricole on its acquisition of payments firm Linxo Group in January 2020.

Alongside Software, Bryan Garnier’s core sectors include Energy Transition and Sustainability, Healthcare, Industrial Tech, NextGen Consumer and Business and Tech-Enabled Services. Bryan Garnier’s mission of investment banking for a better future continues to drive the firm as it backs disruptive companies and their investors that are providing solutions to some of the world’s most important challenges.

MEDIA CONTACTS

Desiree Maghoo, Questor Consulting

dmaghoo@questorconsulting.com

07772255740

Sophie Mills, Questor Consulting

smills@questorconsulting.com

07971406258

Cell therapy Innovation: CAR T

bethsabee gresse

Our guest

Autolus

BioNTech

Cellectis

Evotec

Galapagos

Date: Nov 14th from 2:00pm - 5:30 pm CET

Join our analysts on fireside chats about the present and future of CAR T therapies in oncology. These conversations are a unique opportunity to get a comprehensive update and learn more from the European companies leading innovation in the field.

Hidden value in consumer healthcare

The consumer healthcare market has reached an inflection point, with abounding opportunities for global players to emerge in a highly fragmented market.

Bryan Garnier’s latest White Paper “Hidden Value in Consumer Healthcare” showcases trends in this rapidly evolving market. Opportunities for investors emerge in a still fragmented sector due to increasing consumer demand. The array of recent consumer health and OTC business spin-offs from large pharma companies epitomize the renewed interest in capital allocation towards this growing industry.

Following widespread research in the consumer healthcare space, we identify 5 key success factors based on current trends and key success stories that will mold the next generation of leaders. We expect winners in this sector to be ones that break free from the pharma mindset into a consumer-centric approach. Today’s eco-conscious self-care consumers increasingly desire natural products, while omni-channel strategies for distribution tie-up with Gen Z and millennials’ mindsets. To emerge as a leader, companies furthermore need to think strategically about opportunities for M&A.

Request this whitepaper to see the key success factors that will shape future leaders in this increasingly hot market, which is set to grow to a size of USD 450bn by 2030.

Download report

Please complete the form below to receive the report.

Opportunities in the fast-growing EV charging market

In the next 10 years, demand for EV charging points is likely to grow by 40% to more than 35 million units in Europe alone.

EV charging plays a crucial role in the transition towards cleaner transportation. Although adoption of EVs is increasing, the lack of charging infrastructure and range anxiety remain a major headwind to the growth of this market, requiring significant investment in the years ahead. European and domestic regulators have implemented different measures to accelerate the transition to e-mobility, notably subsidies and deadlines for the phasing out of internal combustion engines (ICEs). The availability and accessibility of charging infrastructure across private and public spheres is a fundamental pre-requisite.

Following widespread research, including contact with companies across the EV ecosystem this whitepaper focuses on the three main segments of EV charging: original equipment manufacturers (OEMs), charging point operators (CPOs) and e-Mobility service providers (e-MSPs). This paper also identifies what we consider to be the next technological disruptions in the EV charging market: smart charging, data aggregators and next-gen batteries. These innovations will allow new business models to develop, such as vehicle-to-grid (V2G) and vehicle-to-home (V2H) charging.

Download this whitepaper to find out more about this exciting growth sector that is accelerating the adoption of EVs and the shift to cleaner transportation.

Download report

Please complete the form below to receive the report.

Partner Olivier Beaudouin interviewed by IFR on Bryan Garnier’s leadership in the Energy Transition and Sustainability sector

Partner Olivier Beaudouin interviewed by IFR on Bryan Garnier’s leadership in the Energy Transition and Sustainability sector

International Financing Review (IFR) has written a piece highlighting Bryan Garnier’s leadership in the Energy Transition and Sustainability sector. From insect protein to hydrogen, the piece highlights some of the landmark transactions that Bryan Garnier has advised on and the sector knowledge that our bankers leverage to ensure the best outcome for disruptive sustainability companies and their investors.

Olivier explains the unique financing structures that Bryan Garnier advises on that ensure that companies have the right combination of investors on board so that they can scale up.

The piece highlights Bryan Garnier’s position as the go-to bank for European disruptors and their investors. “We generally act as the lead adviser on transactions as we’ve been in this space for 15 years so we leverage our long-standing and extensive relationships with the strategic and private and public financial ecosystem globally very well, while keeping the agility of an entrepreneurial firm,” Beaudouin said.

Read the full article here:

For more information, please contact Olivier Beaudouin

Olivier Beaudouin

"2021 was a peak year" Interview with Falk Müller-Verse, Managing Partner, Bryan, Garnier & Co.

For the seventh year in a row, big-name growth investors have identified the top 50 list of the fastest-growing venture-backed technology companies in Europe as part of the Tech Tour Growth - all with the potential to become "Unicorns" in the foreseeable future.

Falk Müller-Veerse headed the selection committee - in this interview he talks about the winners, potential Unicorns and the impact of the Ukraine war on IPOs.

Goingpublic: Mr Falk Müller-Verse, Bryan Garnier is the world's leading full-service investment bank for European technology and healthcare companies. What exactly is your mission?

Falk Müller-Verse: Our corporate clients are active in high-growth sectors with partly disruptive business models. We want to help them become global champions by accompanying them through all phases of the life cycle and providing them with access to public and private capital.

In your opinion, was 2021 a good year for investment banks?

Müller-Verse: Yes, 2021 was a record year - for us, as it certainly was for many investment banks. Bryan Garnier alone advised on 35 M&A deals with leading private equity investors and global companies last year, as well as 36 growth financings with a total volume of EUR2.75bn.

With the Tech Tour Growth Award, you honour companies that have the potential for a stock market value of over EUR1bn. Can you give us examples of companies that you have successfully accompanied to the stock exchange?

Müller verses: I hardly know where to start. Biontech is without doubt especially well known in this country. We accompanied the Mainz-based biotech company during its IPO in the USA. More recently at the end of May, we took the hydrogen company Lhyfe to Euronext in Paris - in a very difficult market environment.

Who are the 2022 winners of the Tech Tour Growth Award and what potential do you see in these companies?

Müller-Verse: Of the three winners in the categories Digital, Sustainability and Health, I would like to highlight the two companies in the first two areas: In the context of sustainability, the Dresden-based hydrogen technology provider Sunfire made it to first place. Hydrogen is one of the most important technologies for securing our energy supply in the future. The winner in the digital field was German-Finnish company IQM, which develops the hardware for quantum computers with special tasks. IQM carries the hopes of many industrial groups that would like to push the development of these computers for industrial applications.

How do you see the IPO market in 2022/2023 or what impact do you think the Ukraine war and the still present Covid-19 crisis will have?

Müller-Verse: When share prices of big tech companies collapse, this naturally also affects IPO sentiment and ultimately start-up valuations. We have already seen significant corrections here and will probably continue to see them. In the wake of the Ukraine war, many IPO plans have been officially put on hold for the time being, but there is definitely some movement behind the scenes. In the medium term, however, the outlook remains good, also for IPOs - after all, this is the preferred way of financing growth if entrepreneurs want to retain their independence.

Thank you very much for the interview.

Bryan, Garnier & Co: an independent investment bank dedicated to growth companies

Specialised in growth sectors linked to innovation and new technologies in various business sectors, the independent investment bank Bryan, Garnier & Co has been helping European companies to grow and develop for 25 years. Interview with Greg Revenu, one of the co-founders of the firm.

Can you tell us a little about the business of the independent bank Bryan, Garnier & Co?

Bryan, Garnier & Co is a European investment bank with a unique business model, largely inspired by the American investment banks that have shaped the US technology sectors since the 1980s.

The business model is distinctive in several respects: firstly, it has an international approach organised around specialised industrial sectors; secondly, it has a broad transactional capacity (unlisted fundraising, IPOs in Europe and the US, convertible issues, mergers and acquisitions, research, trading) which guarantees our independence in the advice we provide and leads us to position ourselves across the entire development curve of companies, from start-up to large-cap through all the intermediate stages. Finally, the model stands out for the independence linked to our partnership structure.

Indeed, what sectors does your investment bank operate in?

Our investment bank is present in various technology-related sectors; through it we cover several areas such as health, especially biotechs and medtechs, information technology (from enterprise software to cybersecurity via robotics or space), but also the energy transition and the environment in the broader sense, as well as service activities related to these sectors (“tech-enabled services”).

Bryan, Garnier & Co. also contributes its expertise in ‘NextGen consumers’, whether through e-commerce, new consumer activities, and so-called ‘next generation’ products.

In short, we specialise in sectors related to innovation and new technologies, through which we develop extremely high-level expertise and knowledge.

In which countries does your investment bank operate?

Unlike other players, we have a pan-European focus. After starting out in London, we extended our physical presence to other countries on the continent such as France, Germany, Scandinavia and the US.

However, as I said, we are organised by sector of activity and not by geography, with teams working in all regions according to their sectoral or transactional expertise.

How do you manage to stand out today?

Our bank offers an extremely broad spectrum of transactional tools and know-how. Very often, firms are specialised in a specific type of transaction (fundraising, M&A, capital markets), whereas we want to offer a very broad spectrum of transactions in the different sectors we cover. We could even say that we are agnostic in this respect, having a very strong level of sector specialisation!

We have also chosen not to specialise in terms of size, we work with large clients as well as smaller structures and are committed to the companies that we assist at each new stage of development

More specifically, what do your clients look for when they turn to your investment bank?

Our objective is to identify companies that are growing and developing rapidly, either organically or through acquisitions in Europe, and to support their growth over the long term. We provide companies, their managers and shareholders an ecosystem that enables them to facilitate this development by securing financing for their growth, irrespective of what type, or by assessing transactional or liquidity opportunities. Our research activities enable them to benefit from permanent insights into the dynamics of their markets, as well as to gain visibility in the financial ecosystem.

We make all our transactional capabilities available, as well as one of the largest teams in Europe with over two hundred professionals specialised in the wider technology fields, all from a long-term perspective.

What challenges is Bryan, Garnier & Co facing today?

We are about to celebrate our 25th anniversary in a few months. Within a quarter of a century, the world in which we find ourselves has changed massively.

Today, we are talking about the metaverse, developing vaccines in just two years for a pandemic that, a few decades ago, would have decimated almost half the world’s population. Bryan, Garnier & Co. has been affected by all these changes in the world, but has also been a contributor. The challenge is to remain a contributor to the great changes the world is about to experience.

We are therefore now looking at the new challenges for the world of tomorrow, both in terms of climate issues and technological issues in the broader sense.

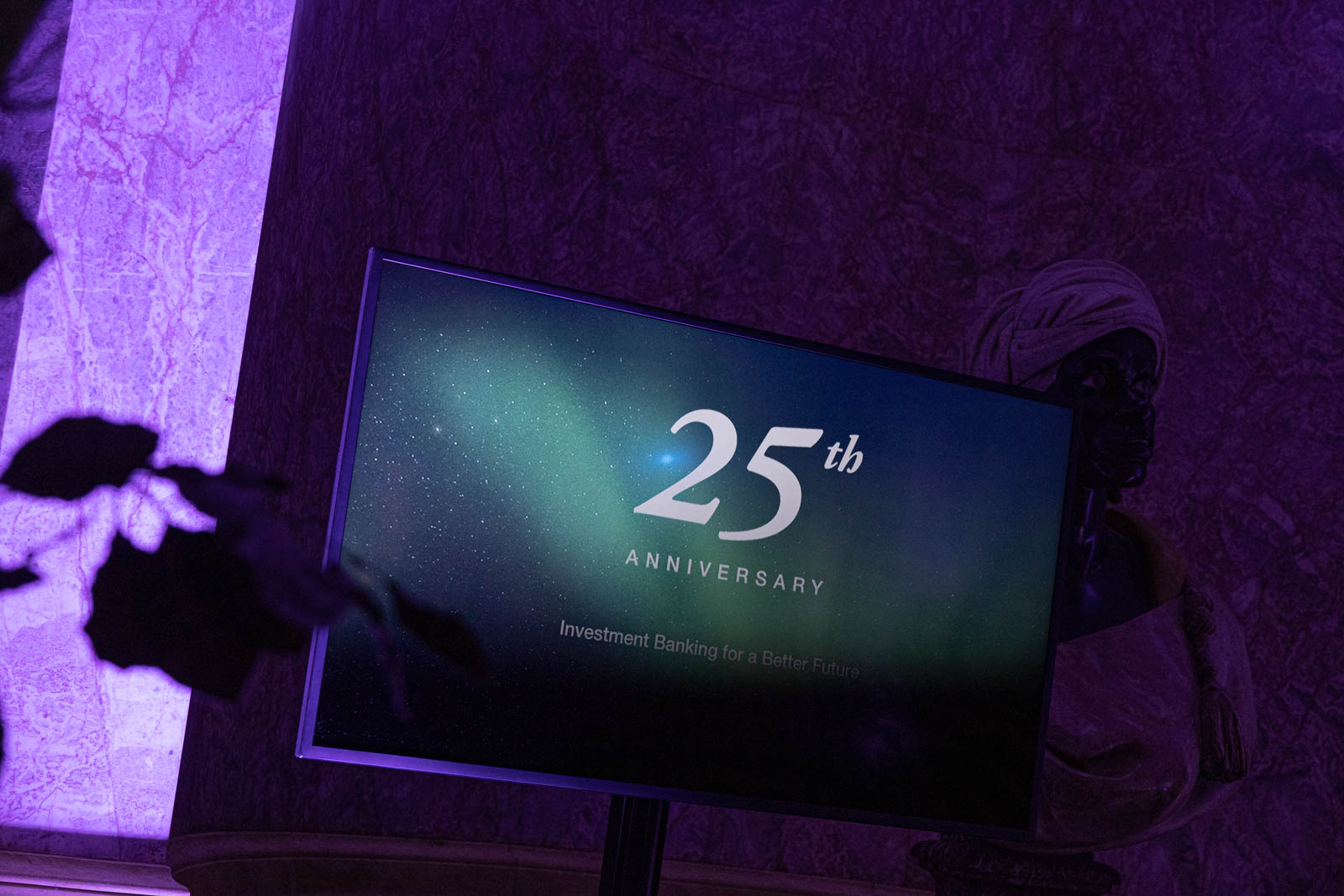

Celebrating 25 years of backing disruptors

On Thursday 23 June 2022, Bryan Garnier celebrated its 25th year of backing disruptors with an anniversary event at the Petit Palais in Paris. The event was a celebration of the achievements of team Bryan Garnier, of our clients who have played an essential part in our journey so far and of the innovation across technology and healthcare that we have been backing for the last 25 years.

We were thrilled to welcome our guests and share with them an exlusive NFT, specially commissioned by Bryan Garnier to mark this milestone. In addition, Andrew McAfee, a research scientist at MIT and best-selling author on AI and digital technology delivered the keynote address and we were delighted to invite Bryan Garnier client Matthieu Masselin, CEO of Wandercraft, which manufactures revolutionary exoskeletons allowing patients to walk again, to speak. Mattieu was presented with an award for 2021 Deal of The Year, marking Bryan Garnier’s ongoing commitment to backing companies that are building a better future.

A huge thank you to all of our clients, the Bryan Garnier team and to everyone we have worked with over the last 25 years. We are looking forward to a bright future as we continue to back disruptors, driven by our purpose of investment banking for a better future.